[ad_1]

On March 25, 2022, President Joe Biden introduced an settlement committing the U.S. liquefied pure gasoline (LNG) trade to produce an extra 15 billion cubic meters (bcm) of LNG to Europe by the rest of the yr. The settlement additionally envisions U.S. LNG rising provide to Europe to 50 bcm by 2030, equating to roughly one-third of the European Union’s (EU) gasoline imports from Russia in 2021. Apparently, whereas properly acquired by European allies and the U.S. LNG trade, the announcement might by no means have been mentioned with the trade. One main U.S. LNG participant, Charif Souki, the pinnacle of developer Tellurian, instructed The New York Occasions, “I don’t know how they’re going to do that, however I do not need to criticize them, as a result of for the primary time they’re making an attempt to do the precise factor.” The query now could be how will the U.S. authorities, in a free market, direct commercially unbiased corporations to ship LNG to Europe?

Background

The U.S. LNG trade emerged in 2016 when Cheniere turned the primary firm to export LNG into the world market. At the moment the U.S. is without doubt one of the high three international LNG producers and is about to change into the primary provider later this yr, surpassing LNG export giants Qatar and Australia. The U.S. LNG trade has grown by reshaping the traditional LNG enterprise with a pointy deal with commercialization. The trade has been compartmentalized with corporations specializing in liquefaction and product gross sales, leaving upstream useful resource growth and the midstream to others. The event and development of liquefaction crops are actually commoditized.

Commercially, the U.S. LNG challenge builders have offered their product primarily to portfolio gamers, resembling Shell, BP, Whole, Trafigura, and Vitol, and the Asian market, retaining little uncontracted LNG quantity for themselves to be offered on the spot market. The long-term contracts with excessive credit score consumers have been required to underpin challenge financing. With little uncontracted spare LNG quantity and long-term contracts, the challenge builders have little flexibility to direct materials volumes to the European market right this moment.

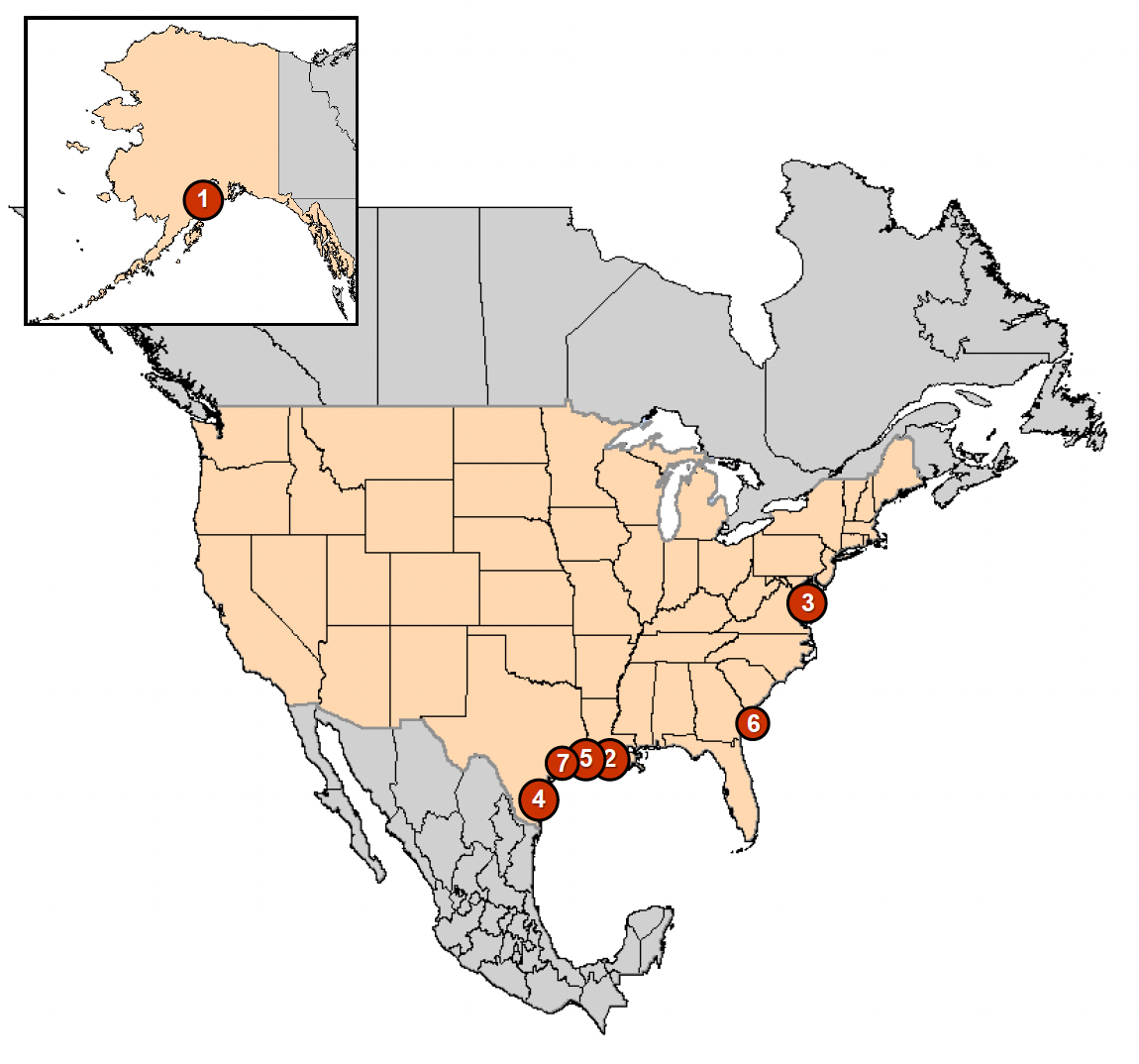

Present North American LNG export terminals

- Kenai, AK: 0.2 Bcfd (Trans-Foreland)

- Sabine, LA: 3.5 Bcfd (Cheniere/Sabine Move LNG –Trains 1-5)

- Cove Level, MD: 0.82 Bcfd (Dominion–Cove Level LNG)

- Corpus Christi, TX: 1.44 Bcfd (Cheniere –Corpus Christi LNG Trains 1, 2)

- Hackberry, LA: 2.15 Bcfd (Sempra–Cameron LNG, Trains 1-3)

- Elba Island, GA: 350 MMcfd (Southern LNG Firm Items 1-10)

- Freeport, TX: 2.13 Bcfd (Freeport LNG Dev/Freeport LNG Growth/FLNG Liquefaction Trains 1-3)

Trying forward: The LNG sellers

The U.S. LNG sector is poised for extra development with a number of tasks in growth and others within the development section. A minimum of six tasks plan to take the ultimate funding determination (FID) in 2022. Ought to that happen, the U.S. would add a minimal of 84.0 million tons each year (Mtpa) by 2026. Nevertheless, the fact is that a number of tasks won’t attain FID as a consequence of challenge execution uncertainty and lack of offtake agreements. Actually, it’s possible that solely 25% (21.7 Mtpa) of the forecasted 84.0 Mtpa will materialize in time to ship LNG to the European market by 2026.

The 2 essential challenges tasks face are challenge execution, which drives challenge value, and offtake agreements, which offer challenge income. Combining the associated fee and income determines the financial return. Undertaking execution depends on provide chain administration, together with tools, materials, and craft sources. All three classes are at the moment experiencing challenges, shortages, and pressures that drive challenge prices increased and threaten supply dates. Whereas LNG costs are excessive now, long-term pricing anchors income and long-term costs are decrease than present spot costs. As such, challenge economics are challenged.

The U.S. LNG challenge queue is lengthy, with tasks in varied levels of growth. New tasks haven’t secured offtake agreements for 100% of the LNG quantity, which suggests that some volumes are nonetheless “on the market” to European consumers. Two main tasks at the moment underneath development, the Qatar Vitality/ExxonMobil Golden Move LNG (first LNG 2024) in southeast Texas and the Shell-led LNG Canada (first LNG 2024) in British Columbia, took FID with out contracting their LNG volumes. As an alternative, the events dedicated to take LNG volumes into their portfolio. The 2 tasks will ship greater than 29.0 Mtpa into the market and provide the European market much-needed LNG within the close to time period, supplied, after all, consumers and sellers attain a industrial settlement on gross sales worth, contract phrases, and tenor.

To date, 29.0 Mtpa will come onto the market from the 2 tasks underneath development (Golden Move LNG and LNG Canada), and an extra 21.7 Mtpa by 2025 from tasks which have an affordable likelihood of reaching FID in 2022. This equates to roughly 50.7 Mtpa of recent LNG volumes anticipated to enter the market by 2025. Of that complete, 29.0 Mtpa have been uncontracted at challenge FID. Contracted volumes and the consumers for the 21.7 Mtpa to be delivered from tasks anticipated to succeed in FID in 2022 are unknown. This means that important volumes of North American LNG are anticipated to be obtainable to European consumers for supply in the course of this decade. One other 62.0 Mtpa can probably mature; nonetheless, these tasks face important industrial challenges. Reaching FID in 2022 might not transpire, thus delaying first LNG dates to the late 2020s, assuming they attain FID in any respect.

U.S. LNG builders are additionally making an attempt to decipher the Biden administration’s power technique. With preliminary efforts centered on limiting any hydrocarbon-based challenge growth, the trade ready for the challenges of allow approvals, challenge sanction, and modifications to working laws. Over the previous month, nonetheless, the administration has publicly provided U.S. LNG to Europe however continues to restrict upstream permits. As U.S. LNG crops develop, extra gasoline sources might be wanted. Thus, upstream permits might be important to long-term U.S. LNG provide development.

Trying forward: The LNG consumers

The market wants to soak up any extra U.S. LNG volumes. For the reason that Biden administration said elevated volumes would go to the European market, one should ask the place the LNG consumers are. As famous, long-term contract pricing should assist ample financial returns for challenge builders, and U.S. LNG provide might be competing with forecasted new Qatar LNG provide, which can possible have a decrease value foundation. Portfolio consumers will proceed to take competitively priced LNG, as will the traditional Asian tram line consumers. The European consumers might want to compete for volumes, and U.S. LNG might want to compete for consumers.

A number of challenge builders have expressed concern over the long-term nature of the European market. Whereas European consumers have lately attended U.S. LNG trade occasions, the EU doesn’t maintain a constant view. Some nations have expressed concern about greenhouse gasoline emissions and the carbon footprint of recent LNG volumes. Others have commented that termination of Russian piped gasoline provide will truly scale back greenhouse gasoline emissions due pipeline leaks. Undertaking builders are involved that the EU will search U.S. LNG in the course of the Ukraine disaster however might not want long-term LNG provide, opting to revert to “greener” choices as soon as the disaster passes and leaving U.S. LNG suppliers with short-duration contracts. U.S. LNG suppliers have raised questions on whether or not that is only a non permanent change or if the EU is shifting again to gasoline and slowing its inexperienced power technique. Smarter and probably smaller LNG tasks (3-5 Mtpa) that require two to 3 offtake contracts to succeed in FID might have a aggressive benefit over large-scale standard LNG tasks (10-12 Mtpa), which require important offtake volumes (7-10 Mtpa) contracted to safe FID and take longer to assemble.

Conclusion

A window of alternative exists for U.S. LNG challenge builders. The Biden administration promise to ship extra U.S. LNG to Europe would require a rise in LNG export capability. Corporations which have a website, robust feed gasoline provide technique, federal and state permits in hand, and an engineering, procurement, and development contract able to execute can transfer rapidly to make sure first LNG supply previous to the 2030 deadline. The U.S. LNG challenge portfolio can ship extra LNG volumes to Europe by 2030 however these challenge builders want to make sure challenge supply/first LNG dates previous to 2030 and safe offtake contracts with the European consumers.

Till the mid-2020s, European consumers might want to safe LNG provide from the worldwide spot market, Asian prospects who could also be lengthy in provide, portfolio gamers, and U.S. LNG suppliers with minimal spare volumes. Whereas the Biden administration announcement is constructive for the trade, there are a lot of steps to take earlier than the promised LNG volumes materialize.

Wayne Ackerman has greater than 30 years’ expertise within the upstream exploration and manufacturing sector and main capital challenge growth, together with LNG. He’s additionally the founder and president of Ackerman and Associates World Consulting, LLC, and a member of the Advisory Council for MEI’s Program on Economics and Vitality. The views expressed on this piece are his personal.

For extra particulars on authorized however not but constructed and proposed LNG export terminals, please see the complete set of LNG export maps from FERC.

Picture by Mark Felix/Bloomberg by way of Getty Pictures

[ad_2]

Source link

{kind=link}