[ad_1]

The eurozone’s newest financial progress figures are slightly higher than anticipated. This group of 19 EU nations grew 2.2% within the second quarter of 2021 in comparison with the primary quarter, partly because of first rate performances from Spain and Italy.

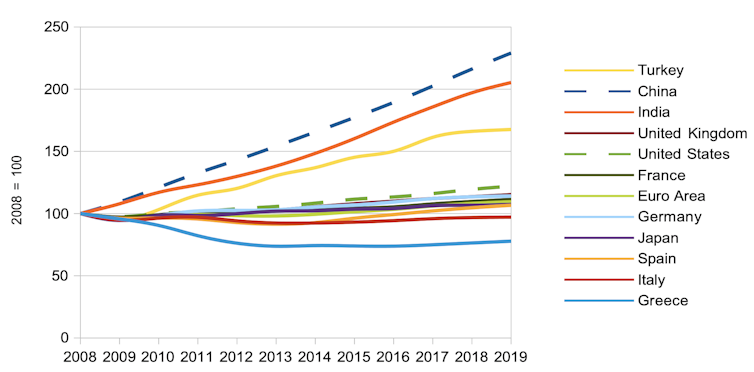

However whereas the US and Chinese language economies are each now larger than their 2019 peaks, the eurozone is 3% off that achievement. And while you look extra broadly on the state of the eurozone, this seems to be solely the tip of the iceberg.

Covid-19 nonetheless overshadows the whole lot around the globe, however nations are more likely to recuperate at completely different speeds as soon as we get again to some form of normality. This may rely on the construction of their economies, the effectiveness of their restoration insurance policies, and the way they cope with excessive sovereign money owed and a foreseeable mixture of weakish progress and inflation. However for a number of causes, the eurozone significantly worries me.

Ghosts of the previous

The primary is the eurozone’s bleak efficiency for the reason that international monetary disaster of 2007-09. It took six years to regain its 2008 GDP degree, and a few members did even worse: Spain and Portugal took virtually a decade, and Italy and Greece have but to get there.

When Covid broke out, the eurozone progress charge remained properly under its long-term trajectory. It was behind the US and UK, each of whom have been hit more durable by the worldwide monetary disaster, and even worse in comparison with the main rising economies. Neither was this a one-off. Trying on the previous 5 recessions, the eurozone nations have been successively slower to recuperate from each.

GDP by nation since 2008

Muhammad Ali Nasir

Since 2008, the ECB has tried quite a few measures to enhance progress. Like most main powers, it has carried out loads of quantitative easing (QE), which entails creating cash to purchase sovereign bonds and different monetary belongings. It has sought to prop up its retail banks in numerous methods, whereas additionally pioneering destructive rates of interest and giving the markets extra ahead steerage about financial coverage.

Famously in 2012, then ECB president Mario Draghi stated he would do “no matter it takes” to save lots of the euro. This ahead steerage stored the euro steady, however the identical can’t be stated of progress.

Poor coverage and low ammunition

Coverage errors are partly guilty for this. With the good thing about hindsight, the eurozone went into the worldwide monetary disaster with lending charges on the low facet, so had much less room to chop than different areas. It was additionally extra reluctant than central banks just like the Financial institution of England and US Federal Reserve to begin QE, preferring to deal with curbing inflation and making the euro “stabil wie die mark” (steady just like the German mark). The ECB didn’t unveil a QE programme till 2015.

International locations with the capability to spend to stimulate their economies, corresponding to Germany, France and the Netherlands, additionally did too little. Spain’s stimulus was poorly designed, whereas Italy was extra serious about balancing its books on the time. Too quickly after the disaster struck, austerity then turned the precedence for the entire eurozone.

A associated downside has been private and non-private funding. In middle-income EU areas, funding charges fell by about 14% between 2002 and 2018. In thrifty Germany, private and non-private mounted investments declined as a share of GDP for many years, regardless of an enormous surplus in public spending.

Earlier than Covid hit, EU infrastructure funding was at a 15-year low, with the best declines in areas that have been already lagging. Initiatives meant to assist, such because the European Financial Restoration Plan of 2008 and the European Fee Funding Plan in 2014, have been too little.

The general end result was that weak point: Germany and the eurozone as a complete have been exhibiting 0% progress on the time of the Covid outbreak, whereas Austria, France and Italy have been all contracting barely. In response, the ECB had reduce its predominant rate of interest by 0.1 share factors to -0.5% in September 2019, and restarted month-to-month QE to the tune of €20 billion (£17 billion) from November 1 of that 12 months – the date Christine Lagarde turned ECB president.

The eurozone financial system was due to this fact needing life help even earlier than the pandemic – certainly, lots of the ECB’s different unconventional help measures have been in place all through. Tellingly, the ECB’s solely new measure in the course of the pandemic has been a brand new type of cheaper refinancing for banks. It raises the prospect of the ECB operating out of the ammunition wanted to maintain stimulating the eurozone’s sickly financial system.

Self-discipline über alles

Lastly, some eurozone members are obsessive about the EU’s fiscal guidelines round low nationwide debt and low deficits. The Monetary Occasions could have reported in March 2020 that “Germany tears up fiscal rule e book to counter coronavirus pandemic”, however there are already calls by influential figures corresponding to Bundestag president Wolfgang Schäuble to return to fiscal self-discipline.

A rush to austerity 2.0 is a luxurious that the EU can’t afford. To cite one thing typically attributed to Albert Einstein, madness is doing the identical factor over and over and anticipating completely different outcomes.

For various outcomes, the ECB ought to stand its floor on financial easing and, just like the Fed, keep away from giving in to inflationary pressures which can be more likely to be brief time period by elevating charges or paring again QE.

In the meantime, the fiscal guidelines want loosening to correspond to financial realities. The temptation have to be prevented to throw the nations within the peripheries underneath the austerity bus once more, one of many predominant causes of the eurozone disaster of the early 2010s.

Surplus nations, significantly Germany, ought to revive spending in infrastructure, schooling and know-how. The EU’s €750 billion Subsequent Era EU funding plan will belatedly kick in later this 12 months, however identical to the 2 earlier EU restoration packages, will in all probability not be sufficient by itself.

With an unimpressive observe file on restoration, inherently weak economies, an obsession with fiscal guidelines and the prospect of the ECB operating out of ammunition, the choice may very well be a second misplaced decade. What that might do to the eurozone and the EU, it could be higher to not discover out.![]()

Muhammad Ali Nasir, Affiliate Professor in Economics and Finance, College of Huddersfield

This text is republished from The Dialog underneath a Inventive Commons license. Learn the unique article.

[ad_2]

Source link

{kind=link}