[ad_1]

US shares proceed their weak spot this week, with the S&P 500 touching down at $4136, sitting proper at its important assist stage established in mid-March. Volatility is elevated once more close to the latest highs with the VIX sitting at 34 as earnings season hits its midpoint.

When there’s persistent weak spot in shares, everybody comes out of the woodwork to provide you a laundry checklist of the reason why the market is doomed. And there are some actual headwinds to this market which is already at arguably elevated ranges relative to historical past and the financial outlook forward.

Chief amongst these headwinds are:

- Anticipated Federal Reserve tightening

- The Russia and Ukraine warfare

- China COVID lockdowns

- Persistently excessive inflation

So with out additional ado, let’s check out a couple of charts and see what’s happening in markets.

The S&P 500 is sitting proper at its essential assist stage round 412 (or 4120 for futures) and it reached this stage with very sturdy bearish momentum which is a crimson flag for any lengthy setups. The pullback formation we highlighted a couple of weeks in the past has clearly failed and the one wise motive to be lengthy this market is for imply reversion.

It’s all the time essential to remember the fairness market’s tendency to imply revert, as being a composite of lots of of shares, they don’t are likely to have very sturdy momentum on both aspect for too lengthy.

On a relative power foundation, the anticipated is happening. Blue chips within the Dow Jones Industrial Common (represented by the DIA ETF) stay the strongest, whereas the extra dangerous and long-duration belongings like small caps and the NASDAQ 100 are getting hit the toughest. The drought in decrease high quality tech firms in particular is probably going chargeable for a lot of the elevated weak spot within the NASDAQ, as these firms are seeing their beforehand arguably absurd valuations taking an enormous haircut.

Shifting our focus to grease, not a lot of observe has occurred in crude, which stays in it’s weeks-long consolidation sample and ends the week round $104 per barrel.

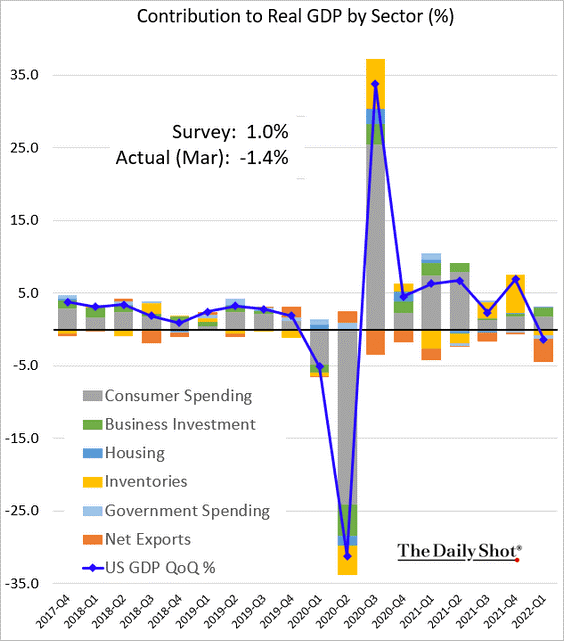

Chart of the Week

To the shock of most, GDP truly contracted throughout the first quarter of 2022, owing to components just like the Russia and Ukraine warfare hitting the availability chain onerous and protracted inflation crushing client confidence:

Final Week’s Information

There have been some massive tales this week:

- Elon Musk supplied to buyout Twitter (TWTR) at $54.20/share and offered $8 billion of Tesla (TSLA) inventory to fund it. The FTC is now investigating the timing of Musk’s SEC filings

- GDP contracted in Q1 2022, declining 1.4% vs. an estimated 1.0% advance.

- Large Tech earnings a combined bag, with Amazon (AMZN) disappointing, Fb (FB) stunning massive time, Google (GOOG) combined, Microsoft (MSFT) combined, Intel (INTC) disappointing, Apple (AAPL) stunning, and though it was final week, Netflix (NFLX) logging an enormous disappointment with many questioning the corporate’s future

- Activision Blizzard (ATVI) shareholders overwhelmingly approve Microsoft acquisition

- The American Affiliation of Particular person Traders sentiment report reveals sentiment at lowest in over a decade

Earnings Subsequent Week

We’re midway by earnings season with lots of the market’s juggernauts like Apple and Google already reporting. At present, the S&P 500 is underperforming expectations, with 0.6% earnings development throughout the reporting firms in comparison with a 5% estimate.

Listed here are a number of the firms reporting this week:

Monday, Might 2:

- Berkshire Hathaway (BRK.B, BRK.A)

- Enterprise Merchandise (EPD)

- Nutrien (NTR)

- CNA Monetary (CNA)

- WEC Vitality (WEC)

- Williams Corporations (WMB)

- NXP Semiconductors (NXPI)

- Mosaic (MOS)

- World Funds (GPN)

- Clorox (CLX)

- Devon Vitality (DVN)

- MGM Resorts (MGM)

- Moody’s (MCO)

- Logitech (LOGI)

- Onsemi (ON)

- CVR Vitality (CVI)

- Chemours (CC)

- Avis Price range Group (CAR)

- Amkor Know-how (AMKR)

- Expedia (EXPE)

- FMC (FMC)

- Diamondback Vitality (FANG)

- Leggett & Platt (LEG)

Tuesday, Might 3:

- BP (BP)

- Marathon Petroleum (MPC)

- Pfizer (PFE)

- American Worldwide Group (AIG)

- Prudential Monetary (PRU)

- Progressive (PGR)

- CNH Industrial (CNHI)

- Starbucks (SBUX

- Cummins (CMI)

- Lear (LEA)

- Eaton (ETN)

- Teva Prescribed drugs (TEVA)

- DuPont (DD)

- Estee Lauder (EL)

- Jacobs (J)

- Illinois Software Works (ITW)

- Murphy USA (MUSA)

- Superior Micro Units (AMD)

- Leidos (LDOS)

- Constancy Nationwide Info (FIS)

- Amcor (AMCR)

- ONEOK (OKE)

- KKR (KKR)

- Edison Worldwide (EIX)

- Biogen (BIIB)

- Andersons (ANDE)

- Yum China (YUMC)

- CenterPoint Vitality (CNP)

- Assurant (AIZ)

- Delek US (DK)

- Molson Coors (TAP)

- CMS Vitality (CMS)

- Franklin Sources (BEN)

- S&P World (SPGI)

- Rockwell Automation (ROK)

- Caesars Leisure (CZR)

- Thomson Reuters (TRI)

- Herbalife (HLF)

- Zebra Applied sciences (ZBRA)

- Restaurant Manufacturers Worldwide (QSR)

- Airbnb (ABNB)

- Public Storage (PSA)

- Match Group (MTCH)

- Lyft (LYFT)

- Further House Storage (EXR)

- MicroStrategy (MSTR)

Wednesday, Might 4:

- CVS Well being (CVS)

- AmerisourceBergen (ABC)

- Vitality Switch (ET)

- Metlife (MET)

- Allstate (ALL)

- CDEW (CDW)

- Cognizant Know-how (CTSH)

- Sunoco (SUN)

- Ebay (EBAY)

- Trane Applied sciences (TT)

- Barrick Gold (GOLD)

- Uber Applied sciences (UBER)

- Brookfield Infastructure (BIP)

- Regeneron Pharamceuticals (REGN)

- Pioneer Pure Sources (PXD)

- Marriot Worldwide (MAR)

- Moderna (MRNA)

- NiSource (NI)

- Yum Manufacturers (YUM)

- Ferrari (RACE)

- Reserving Holdings (BKNG)

- Marathon Oil (MRO)

- eXp World (EXPI)

- Etsy (ETSY)

- New York Instances (NYT)

Thursday, Might 5:

- McKesson (MCK)

- Anheuser Busch (BUD)

- ConocoPhillips (COP)

- CBRE (CBRE)

- Block aka Sq. (SQ)

- Kellogg Comapny (Ok)

- Ball (BLL)

- Intercontinental Trade (ICE)

- Apollo World Administration (APO)

- Penn Nationwide Gaming (PENN)

- Monster Beverage (MNST)

- Zillow Group (ZG)

- DoorDash (DASH)

- Shopify (SHOP)

- ContextLogic (WISH)

- Opendoor Applied sciences (OPEN)

- AMC Networks (AMCX)

- Papa John’s (PZZA)

- Dropbox (DBX)

- HubSpot (HUBS)

- Redfin (RDFN)

- WWE (WWE)

Friday, Might 6:

- NRG Vitality (NRG)

- EOG Sources (EOG)

- Goodyear Tire (GT)

- Below Armour (UA)

- DraftKings (DKNG)

- Cigna (CI)

- Brookfield (BBU)

- Enbridge (ENB)

Financial Releases Subsequent Week

We’ve got an enormous Fed assembly subsequent week, on Wednesday, Might 4. Many are forecasting a larger-than-expected charge hike and this assembly would possibly function one other affirmation that the Fed is shifting ahead with their hawkish tone no matter fairness market weak spot. This could function a check for the Fed, as they’ve traditionally flipped the course away from hawkishness everytime the fairness market responded with weaknesses all through this bull market.

Right here’s this week’s financial information releases:

Monday, Might 2:

- ISM PMI Manufacturing Index

Tuesday, Might 3:

- Job openings and job quotes

- Manufacturing facility orders

Wednesday, Might 4:

- ADP employment report

- FOMC assembly

- ISM companies index

Thursday, Might 5:

- Preliminary and persevering with jobless claims

Friday, Might 6:

- Nonfarm payrolls

- Unemployment charge

- Client credit score

[ad_2]

Source link

{kind=link}