[ad_1]

A founder just lately informed me he would have constructed his firm in another way in one other fundraising market.

Once I requested him what he meant, he replied as a result of capital was so plentiful and accessible at present, he employed dearer individuals, spent extra time growing a product, and invested with an extended time horizon earlier than demonstrating proof of success.

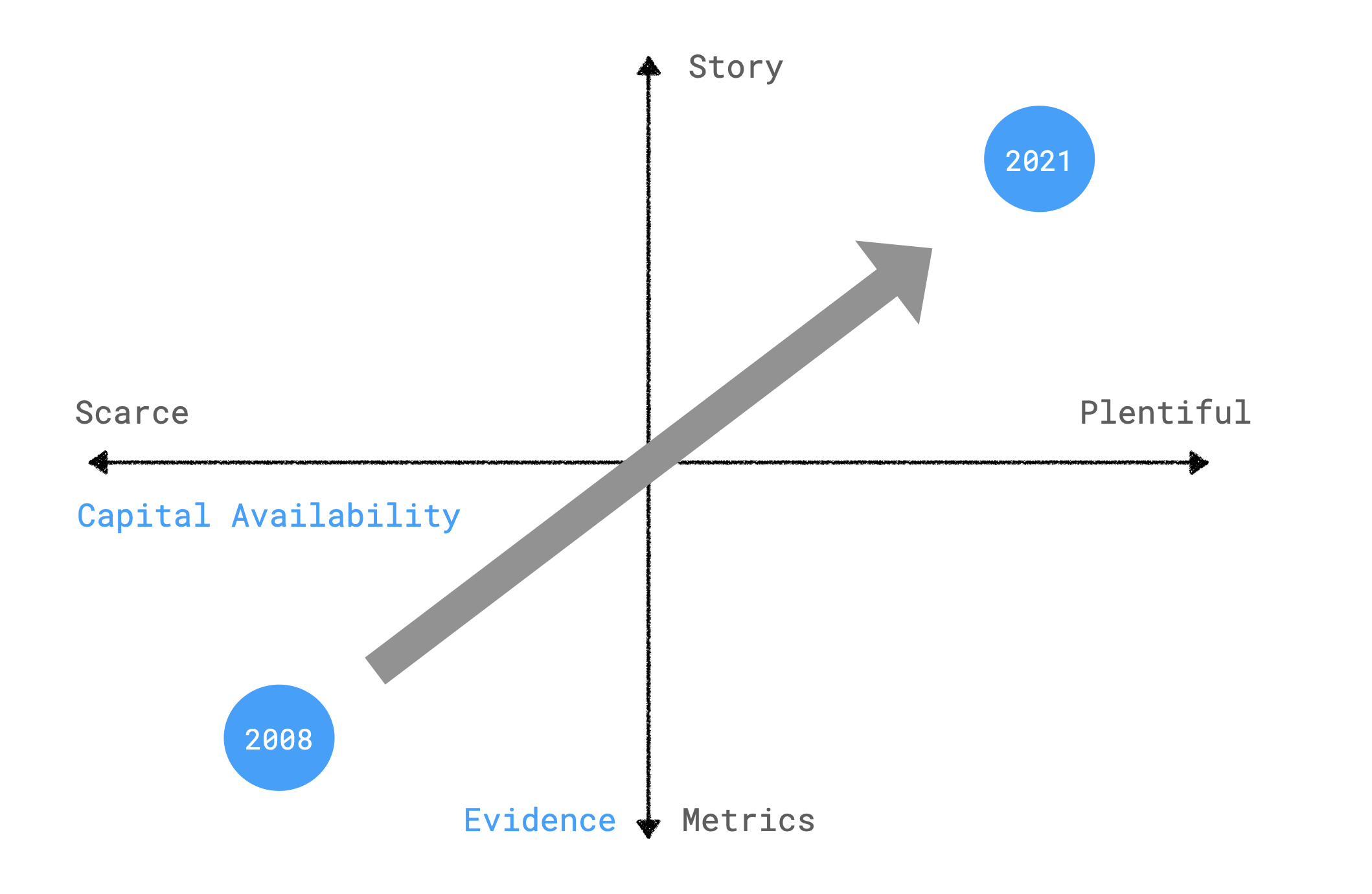

In my pocket book, I sketched this 2×2. Capital availability on the x-axis and proof on the y-axis as an instance his level.

In 2008, tightfistedness dominated the market. Software program startups would wish not less than $1m in ARR to boost capital to muster a small spherical. That meant attending to income as shortly as attainable, or spending as little as attainable to generate revenue. These constraints indicate completely different trade-offs.

The 11 12 months bull market remodeled that dynamic.

As we speak, a narrative is enough to boost a 2008-sized Collection B. Extra capital has inflected the ARR progress curves upward. Ten years in the past, a prime decile software program firm tripled. Keep in mind the triple-triple-double-double? As we speak, it’s a quintuple-quadruple-triple. Lenny Rachitsky published this chart showing top decile companies grow 5x.

Extra capital permits this by allowing sooner hiring, faster software program growth, and maybe much less environment friendly unit economics. (Charting gross sales effectivity by 12 months of IPO can be revealing if so: good thought for a future publish.)

As well as, alongside the best way, buyers and founders started to discover extra capital intensive companies: direct-to-consumer ecommerce, semiconductor firms, actual property possession, multi-year software program growth.

Because the market finds its new regular, I’ve been questioning the place on this 2x,2 the market will land, and if firms might want to redefine PMF in 2022 and 2023? Will companies concentrate on shorter time period milestones once more in additional capital environment friendly classes?

It is dependent upon the depth of the potential recession and the impression to the capital markets. As an investor, I want sooner rising firms: the time to IPO has lengthened to 12 years which may really feel like eons.

Up-rounds arrive faster for hypergrowth firms – spinning the capital flywheel sooner. Make investments -> Develop -> IPO/M&A -> Re-invest.

Given how a lot buyers want sooner progress charges and the large surge in enterprise fund dimension, I don’t count on the ramen and ping-pong days of 2008 to return anytime quickly. However maybe Collection A ARR milestones will retrench considerably, approaching $1m once more, particularly if the downturn takes its time to reverse.

[ad_2]

Source link

{kind=link}